Constructing Efficient Simulated Moments Using Temporal Convolutional Networks

Jonathan Chassot and Michael Creel

Deep Learning for Solving and Estimating Dynamic Models

(DSE2023CH)

August 24, 2023

Our Contribution

- Propose a method to estimate model parameters leveraging

deep learning - Allow for inference using

well-established econometric methods - Provide an

exactly identifying andinformative set of statistics for simulation-based inference - Achieve performance equal to or better than maximum likelihood for small and moderate sample sizes for several DGPs

Motivating Example

- Parameter estimation for a complex data-generating process (DGP)

- Failure of traditional estimation methods (ML, GMM)

Motivating Example

- Parameter estimation for a complex data-generating process (DGP)

- Presence of latent variables

- High-dimensional integrals

- …

- Failure of traditional estimation methods (ML, GMM)

- Intractable likelihood

- Computational constraints

- No closed-form theoretical moments

Methodology

Simulation-based Inference

- Method of Simulated Moments (McFadden, 1989)

- Approximate Bayesian Computation (Rubin, 1984)

- Indirect Inference (Gouriéroux, Monfort & Renault, 1993; Smith, 1993)

- Bayesian Limited Information Estimation (Kwan, 1999; Kim, 2002; Chernozhukov & Hong, 2003)

Method of Simulated Moments

- Use

simulated moment conditions instead of theoretical ones - Match data moments and simulated moments

$$

\hat{\theta}_{\text{MSM}} = \underset{\theta \in \Theta}{\arg \min} \ \left(T^{-1}\sum_{t=1}^T m(x_t, \theta)^{\top}\right) W_T \left(T^{-1}\sum_{t=1}^T m(x_t, \theta)\right),

$$

where $W_T$ is a weighting matrix and

$$m(x_t, \theta) = f(x_t) - \frac{1}{S} \sum_{s=1}^S f(\tilde{x}_t(\theta))$$

with $S$ the number of simulations and $\tilde{x}_t(\theta)$ the data simulated at parameter $\theta$.

Method of Simulated Moments

- …but how do we choose $f(\cdot)$ in

$$m(x_t, \theta) = f(x_t) - \frac{1}{S} \sum_{s=1}^S f(\tilde{x}_t(\theta))$$

Optimal Moment Conditions

- Choosing optimal moment conditions is difficult

- Overidentification leads to high asymptotic efficiency but also to

high bias and/or variance in finite samples (Donald, Imbens & Newey, 2009)

Optimal Moment Conditions

- Choosing optimal moment conditions is difficult

- Overidentification leads to high asymptotic efficiency but also to

high bias and/or variance in finite samples (Donald, Imbens & Newey, 2009)

Theory:

- Gallant & Tauchen (1996) show that the optimal choice of moment conditions corresponds to the

score function (equivalent to MLE)

Optimal Moment Conditions

- Choosing optimal moment conditions is difficult

- Overidentification leads to high asymptotic efficiency but also to

high bias and/or variance in finite samples (Donald, Imbens & Newey, 2009)

Theory:

- Gallant & Tauchen (1996) show that the optimal choice of moment conditions corresponds to the

score function (equivalent to MLE)

Practice:

- Moment selection criteria and algorithms (e.g., Donald, Imbens & Newey, 2009; Cheng & Liao, 2015; DiTraglia, 2016)

- Our work is related to this category

Optimal Moment Conditions

Goal:

- Given a data set $\{x_t \mid x_t \in \mathbb{R}^k\}_{t=1}^T$, generated by our DGP under true parameter value $\theta_0$, we would like to find $f(x_t) \approx \theta_0$

Optimal Moment Conditions

Goal:

- Given a data set $\{x_t \mid x_t \in \mathbb{R}^k\}_{t=1}^T$, generated by our DGP under true parameter value $\theta_0$, we would like to find $f(x_t) \approx \theta_0$

Idea:

- Generate samples $\{\tilde{x}_t(\theta) \mid \tilde{x}_t(\theta) \in \mathbb{R}^k\}$ with $\theta \in \Theta$ and use deep learning to infer $f(\cdot)$, a

mapping from data to parameters

Neural Networks

- Long Short-Term Memory Networks (LSTM)

- Temporal Convolutional Networks (TCN)

Neural Networks

- Long Short-Term Memory Networks (LSTM)

- Hochreiter & Schmidhuber (1997)

- Dominated sequence modelling pre-Transformers (Vaswani et al., 2017)

- Difficulties in modeling long-term dependencies

- Serve as a

baseline deep learning model in this work - Temporal Convolutional Networks (TCN)

- Introduced as WaveNet (van den Oord et al., 2016)

- Fully parallelizable

- Flexible receptive field size

- Serve as the

main model in this work

Benchmark Results

Results for Simple DGPs

- Benchmark our TCNs and LSTMs against MLE for 3 data-generating processes (MA(2), Logit, GARCH(1,1)) where the

likelihood is tractable - Sample sizes 100, 200, 400, and 800

- Comparison across 5'000 test samples for each setting

Conjecture: if the neural networks do well, they will also perform well when the MLE is not available

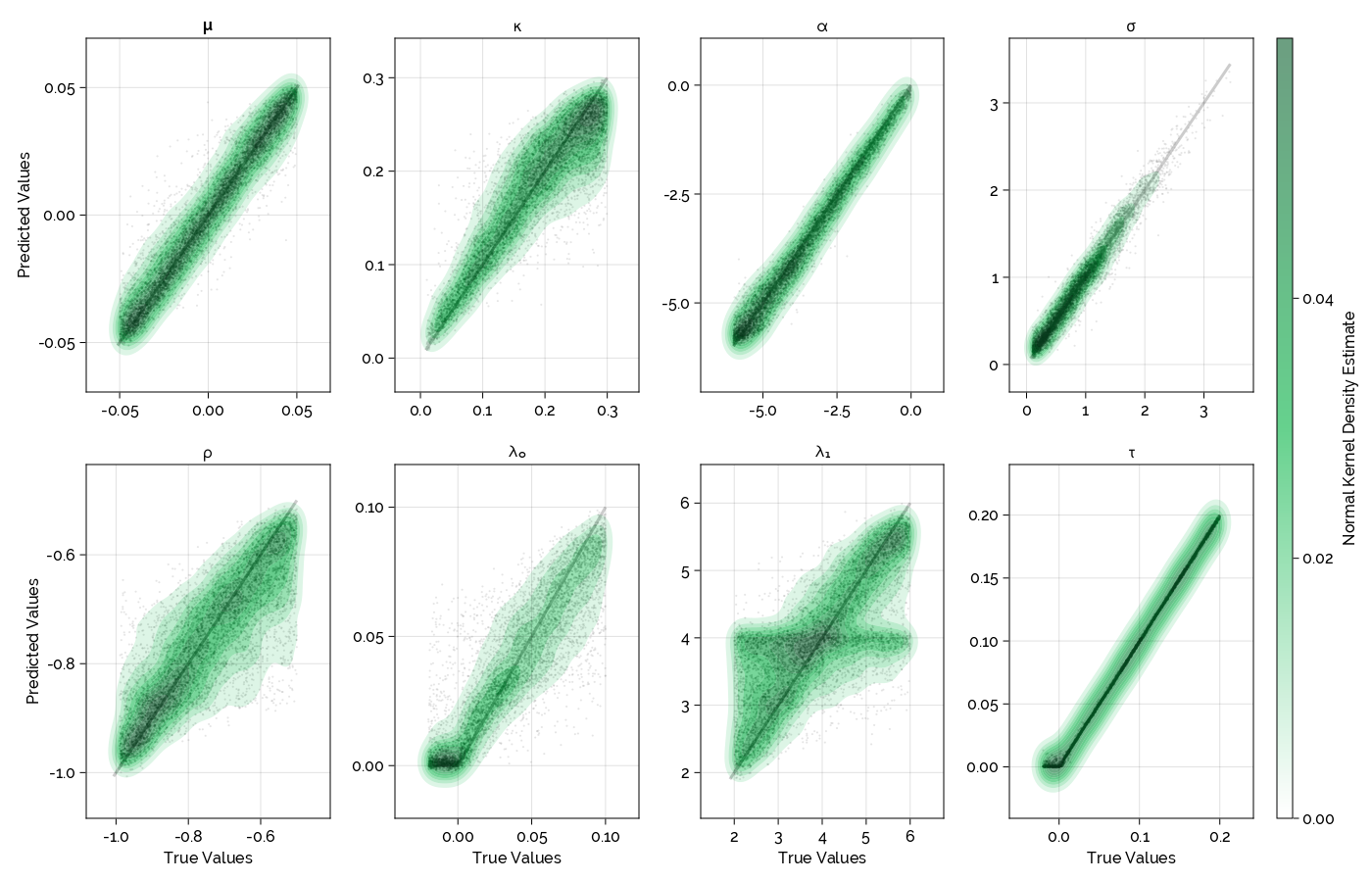

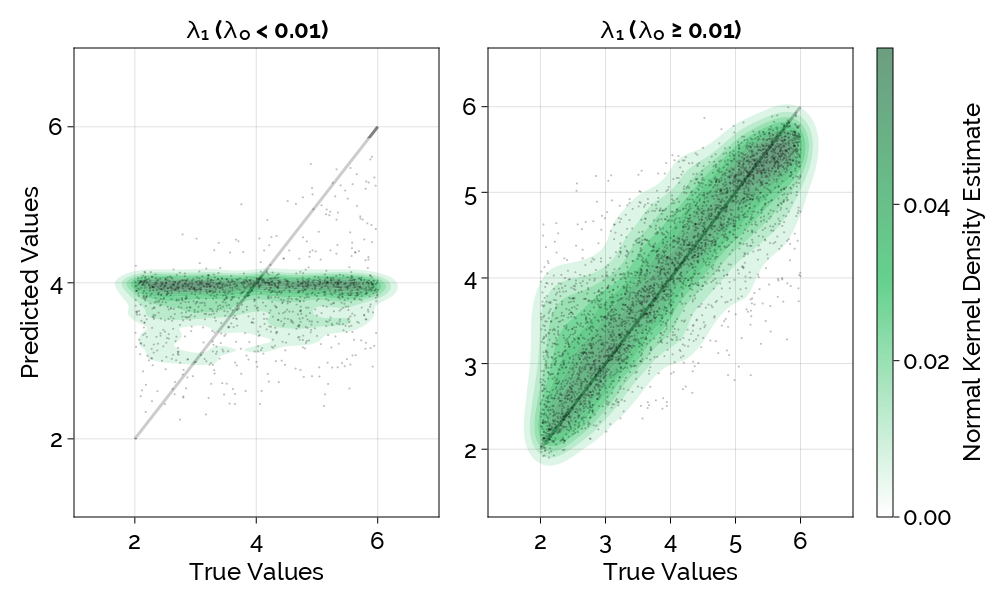

Jump-Diffusion Process

Jump-Diffusion Stochastic Volatility

$$

\begin{align*}

dp_{t} & =\mu \, dt+\sqrt{\exp h_{t}} \, dW_{1t}+J_{t} \, dN_{t}\\

dh_{t} & =\kappa(\alpha-h_{t})+\sigma \, dW_{2t}

\end{align*}

$$

Jump-Diffusion Stochastic Volatility

$$

\begin{align*}

dp_{t} & =\mu \, dt+\sqrt{\exp h_{t}} \, dW_{1t}+J_{t} \, dN_{t}\\

dh_{t} & =\kappa(\alpha-h_{t})+\sigma \, dW_{2t}

\end{align*}

$$

- $p_t$: logarithmic price

- $\mu$: average drift in price

- $J_t$: jump size ($J_t = a \lambda_1 \sqrt{\exp h_t}$) with $\mathbb{P}[a=1]=\mathbb{P}[a=-1]=\frac{1}{2}$

- $N_t$: Poisson process with jump intensity $\lambda_0$

- $h_t$: logarithmic volatility

- $\kappa$: speed of mean-reversion

- $\alpha$: long-term mean volatility

- $\sigma$: volatility of the volatility

- $W_{1t}, W_{2t}$: correlated Brownian motions with correlation $\rho$

Jump-Diffusion Stochastic Volatility

- $\mu$: average drift in price

- $\kappa$: speed of mean-reversion

- $\alpha$: long-term mean volatility

- $\sigma$: volatility of the volatility

- $\rho$: correlation between $W_{1t}$ and $W_{2t}$

- $\lambda_0$: jump intensity

- $\lambda_1$: jump magnitude

- $\tau$: the volatility of a measurement error $N(0, \tau^2)$ added to the observed price

- logarithmic returns

- realized volatility

- bipower variation

Conclusion

Conclusion

- Best case scenario for deep learning

- Once the network is trained, inference is as fast as matrix multiplication

- Limited only in the cost of simulation

- Promising results on three simple DGPs and one moderately complex DGP

- Easy to implement

- Full Julia package under development (already functional):

https://github.com/JLDC/DeepSimulatedMoments.jl